%20(48).png)

ACH used to feel like the most boring payment method in nonprofit fundraising.

Not anymore.

ACH payments are becoming one of the most important drivers of recurring donor retention, payment recovery, fraud prevention, and sustainable fundraising revenue.

Why? Because, as you know well, nonprofits are under pressure from every direction:

- Rising credit card processing fees

- Increased payment fraud attempts

- Rising donor expectations for faster transactions

- Monthly donor churn (lost revenue!) caused by failed payments

- Growing demand for predictable recurring revenue

At the same time, ACH payment adoption continues to grow rapidly across the financial world. The ACH Network processed more than 35 billion payments in 2025, with massive growth in Same Day ACH transactions and business-to-consumer transfers.

So why would this matter to nonprofits?

Because ACH is no longer a back-office finance tool. It's becoming an everyday payment tool, and therefore, a strategic fundraising advantage.

Here are the biggest ACH payment trends to watch.

Same Day ACH is Becoming the New Normal

One of the biggest ACH payment trends right now is the continued rise of Same Day ACH. This means the payment settles on the same business day it's initiated, rather than the standard 1 - 3 business days for regular ACH.

That shift is influencing nonprofit fundraising, too. Same Day ACH gives you faster settlement and better payment visibility.

The speed can improve emergency fundraising campaigns, disaster-response donations, peer-to-peer fundraising payouts, and the reconciliation of recurring donations.

Maybe most importantly, faster ACH processing means reduced uncertainty around incoming revenue. When fundraising and finance teams can see payments quickly, they can make better operational and budgeting decisions.

And as donor expectations continue shifting toward real-time everything, nonprofits that modernize their payment infrastructure will be in a much stronger position than organizations still relying on outdated systems and disconnected workflows.

The 3 ACH Compliance Rules Nonprofits Should Know

If you process ACH donations, you are a participant in the ACH Network. That means Nacha's 2026 rule changes apply to you, even though most of the burden falls on your payment processor.

In practice, there are three things that fall on a nonprofit's side of the fence.

- Get authorization in writing - and keep it! Donors need to give explicit consent before you debit their account, and you need to hold onto that record for two years after the gift stops. A generic "I agree" checkbox won't cut it if there's a dispute.

- Watch your return rates. A return is when an ACH donation fails. It can be the wrong account number, closed account, or disputed charge. Nacha caps them at 15% administrative, 3% overall, and 0.5% unauthorized. Staying well below these thresholds is easy with clean data and a good processor, but it's worth knowing they exist so you can keep an eye on failed payments.

- Know the rules for micro-deposits and Same Day ACH. Both have specific formatting and timing requirements — ask your processor to confirm your setup is configured correctly. They should be able to do that immediately.

These are things a well-designed donor platform helps you manage by default. If you're in the market for a new one, here's a list of more than 25 solid options.

The nonprofits coming out ahead are the ones whose payment processors handle ACH in-house, so the documentation, monitoring, and reporting are already done by the time a regulator or auditor asks.

ACH is Becoming a Bigger Part of Monthly Giving Programs

We can't say it often enough: recurring giving remains one of the most important revenue growth strategies for nonprofits.

And we see it with our clients. ACH payments are playing a much bigger role in sustaining those programs.

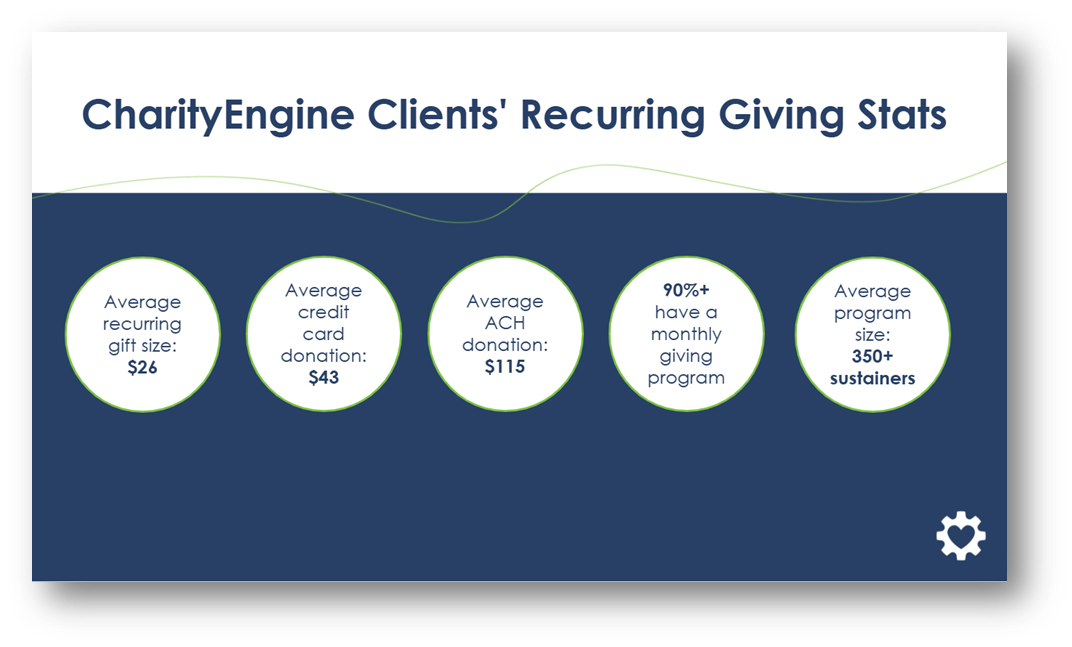

Here's a slide we shared in a recent presentation. Notice that the average credit card donation is $43, while the average ACH donation is more than twice that amount.

Now, many nonprofits rely heavily on credit cards for recurring donations. But therein lies the biggest hidden problem in monthly giving: payment failure.

Cards expire. They get replaced after fraud alerts. Donors get new account numbers. Banks constantly issue replacement cards.

Every one of these disruptions creates friction, increases passive churn, and damages donor retention.

ACH recurring donations are different. Not only do we see larger donations, but bank account information also remains more stable over time, leading to fewer failed payments and stronger long-term donor retention.

For nonprofits focused on growing sustainable revenue (hint: everyone should be), ACH is less about payment processing and more about donor retention infrastructure.

That distinction is important because the real cost of a failed recurring donation isn't just one missed gift. It's the potential loss of years of donor value.

As nonprofits become more sophisticated about recurring revenue and the strategies to maximize it, many are beginning to include ACH payments directly on donation forms.

(As an aside, CharityEngine clients enjoy in-house processing of ACH transfers. It cuts through a lot of red tape and middlemen - and a lot of fees - to offer nonprofits the fastest, most secure option for ACH transfers.)

Expect more nonprofits to optimize donation forms around ACH. It's already happening.

Why More Nonprofits Are Prioritizing ACH Donation Processing

Another major trend we will see is intentional donor steering.

In the past, many nonprofits treated payment methods equally. But today's organizations are becoming more aware of the long-term financial impact different payment types can have on fundraising revenue.

ACH payments typically come with lower processing costs, fewer payment disruptions, and greater stability for recurring payments than credit cards. As a result, more nonprofits are actively encouraging ACH donations during the giving process.

This shift may show up subtly on donation forms. ACH may be positioned as a preferred payment option. Or nonprofits might make bank transfers easier to complete (fewer fields), or explain how ACH reduces transaction costs and protects more donor dollars for the mission.

It's a trend that is most likely among nonprofits focused heavily on recurring giving, like the Wounded Warrior Project, and donor lifetime value. As nonprofits think more deeply about long-term fundraising sustainability, ACH becomes increasingly attractive, not just as a payment method, but as a retention strategy.

Faster Payments Are Changing Donor Expectations

Your donors might not be thinking about ACH payments, and might not even know what ACH means. But their expectations are being shaped by the broader payment experiences they have every day.

Consumers are now used to fast, seamless transactions. Whether it's Venmo, PayPal, or even digital wallets that let us tap to make a purchase, real-time notifications, instant confirmations, and frictionless checkout experiences have become completely normal.

Of course, donors are consumers, so this shift affects nonprofit fundraising, too.

A slow, clunky, or outdated donation process can create hesitation, even if a donor completes the transaction. Now, nonprofits will increasingly need payment systems that feel modern, trustworthy, and flexible.

Given that 89 of every 100 visitors to your donation page will leave without donating, it's clear that donor intent is fragile. And this means that nonprofits should evaluate whether their donation experience aligns with evolving donor expectations. Mobile optimization, faster confirmations, simplified recurring-giving sign-ups, transparent payment messaging, and embedded security all play a role in how donors perceive the giving experience.

Donor experience and payment experience are becoming deeply connected.

How Nonprofits Should Prepare

The ACH trends in this article aren't predictions; they're shaping fundraising programs at the most sophisticated nonprofits. If you want to keep up, here are some ways to start:

-

Look at your current payment mix. What percentage of your recurring donors are on ACH today? If it's under 20%, you have room to grow.

-

Add ACH as a prominent option on your donation form. Not buried, not hidden behind a "more payment options" toggle.

-

Evaluate your processor. Are they handling Nacha compliance for you? Do they offer Same Day ACH? Do they reconcile ACH cleanly inside your CRM?

- Measure ACH retention vs. credit card retention in your monthly giving program. The number might surprise you.

You don't have to tackle all four right now. Start with one, and the improvements start compounding the minute you do.

Every Trend is a Mission Story

"Payments used to be the last thing nonprofits thought about. Now, it's one of the first. Every basis point on fees, every failed recurring gift, every fraud loss - that's money not going to the mission. ACH gives nonprofits a way to protect it." Phil Schmitz, CEO, CharityEngine

Step back from the regulations, the settlement times, the fraud schemes, and the donation form mechanics...just for a minute.

Every trend in this article is the same story told different ways: more dollars going to your mission.

Lower processing fees? More program dollars.

Higher recurring donor retention? A lot more program dollars.

Fewer failed payments? Ditto.

Faster settlement? Better cash flow...for your mission.

Even the new Nacha rules mean you're not losing money to fraud.

And that's what makes ACH more than just a payment method. It makes it a mission-amplification tool wearing a payments uniform.

Build a payment infrastructure that lets more of every dollar you raise go to your mission. ACH is no longer the back-office plumbing of nonprofit payments. In 2026, it's the most strategic lever you have for retention, fraud resilience, and protecting more of every dollar for your mission.

Frequently Asked Questions About ACH Donations

What is an ACH Donation?

ACH (Automated Clearing House) is the U.S. electronic network that moves money directly between bank accounts. An ACH donation is a gift made by transferring funds from a donor's checking or savings account to your nonprofit, without a credit card in the middle. It's the same network that handles direct deposit paychecks, so the infrastructure is mature, secure, and built for recurring transactions.

How long do ACH donations take to clear?

Standard ACH donations settle in 1–3 business days. Same Day ACH, which became widely supported in 2026, settles on the same business day if submitted before the cutoff. For recurring donations, speed matters less than reliability, and ACH wins on both fronts compared to expired or replaced credit cards.

Are ACH donations safe for nonprofits to accept?

Yes, when handled through a compliant processor. ACH transactions are protected by Nacha's operating rules, which include fraud-monitoring requirements that became more rigorous in 2026. ACH transactions often experience fewer payment disruptions and lower chargeback volume than credit cards, reducing failed payments and donor churn.

Can donors reverse or dispute ACH donations?

Yes, but the rules are different from credit cards. Donors generally have 60 days to dispute an unauthorized ACH debit through their bank. Authorized donations they simply changed their mind about are not eligible for the same dispute process, which is part of why ACH chargebacks are less frequent than credit card chargebacks.

Scale Your Fundraising

See how top-performing nonprofits keep a human touch while growing rapidly.

Schedule your 15-minute call-2.png)

%20(7).png)